A full-feature SMSF loan product designed for those looking to build wealth through property within a Self-Managed Super Fund.

* Disclaimer: The information provided herein represents a consolidated summary from all Funders and is not intended to detail any single product offering. For specific product information, please consult your BDM or the Credit team.

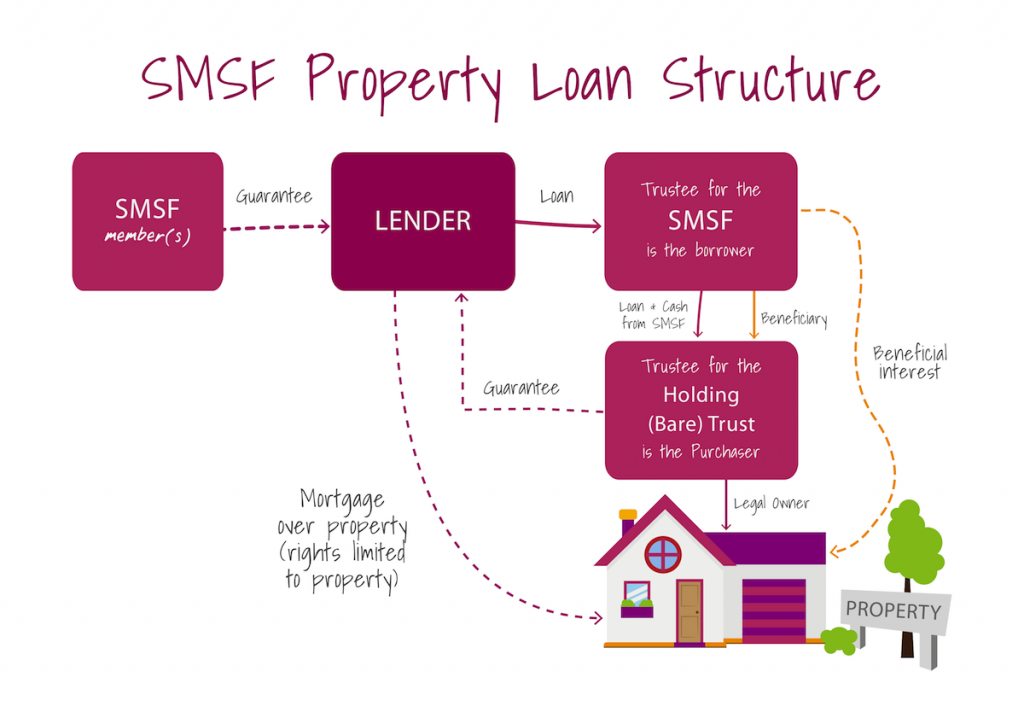

An SMSF loan allows the trustees of the SMSF to borrow money to buy an investment property as part of the SMSF portfolio. The property can be either residential or commercial.

Once purchased, the property is held in a separate custodian trust (bare trust) and any income generated is re-invested into the fund to repay the SMSF loan. When the loan is repaid, the SMSF acquires the deed title. The diagram below shows how this works.

When setting up an SMSF and purchasing investment property, it is recommended to start with at least AUD 200,000. There are the annual accounting and audit fees, typically ranging from AUD 1,000 to AUD 2,000 depending on the complexity of the fund, investment structure, and required professional services.

For those considering an SMSF, it is very important to understand the relevant investment rules and regulations.

Yes, guarantors can take advantage of making additional contributions based on their annual income which will be supported and confirmed by an accountant letter

SMSF retirement benefits can generally be withdrawn tax-free after retirement. Withdrawals are only allowed after meeting a “condition of release.” Members should consult a financial adviser to structure a withdrawal plan.

In addition, in special circumstances (such as severe financial hardship or compassionate grounds), early access to superannuation may be permitted. Specific situations should be handled in accordance with SMSF regulations and relevant documentation.

P: 1800 417 740

E: financial@xin.com.au

Address: Suite 502, 80 Mount Street North Sydney NSW 2060, Australia

©XIN Financial. All Rights Reserved.